Table Of Content

- Navigating Mortgage Pre-approval

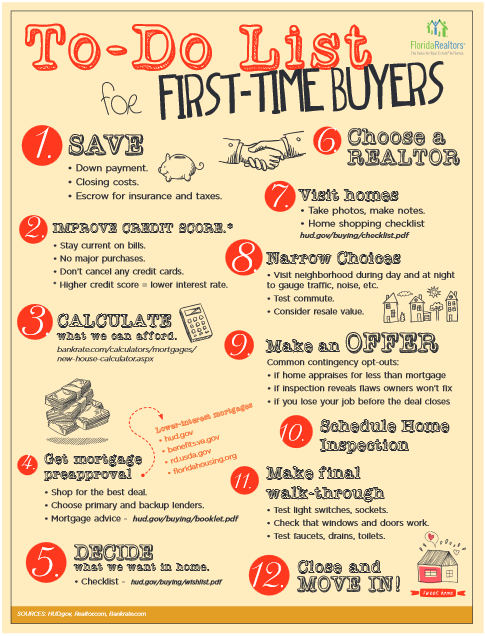

- Step 4: Make an offer and negotiate (up to a week)

- Where Should I Live? 12 Important Factors To Consider

- Enlist The Help Of A Real Estate Professional

- Start looking for homes

- What is a Real Estate Agent and How Do I Find One?

- New home? The costs hidden behind your front door

You can save time and stress, though, by spotting deal-breakers while still in the viewing stage. The second step to purchasing your first home is a crucial one, and that is figuring out how much house you can afford. Perhaps most importantly, a real estate professional can help keep you within your budget. The more you know about the pros and cons of buying a house, the easier it’ll be to make the right decision for you. Read our article to find out what questions you should ask when it comes to choosing the right lender for your needs. Victoria Araj is a Section Editor for Rocket Mortgage and held roles in mortgage banking, public relations and more in her 15+ years with the company.

Navigating Mortgage Pre-approval

In the Los Angeles-area, it’s not uncommon to be bidding against all-cash buyers. That means it is up to the buyer to secure solid financing that is unlikely to fall through during the settlement process. The best time to open a conversation with a lender is before you begin shopping for your home. Finding the right home is often the most time-consuming part of buying a home. This can be especially true in hot real estate markets where there’s more buyer demand than inventory for sale or if you're competing against other buyers, including those making cash offers. Once you're under contract, mortgage underwriting typically takes the next largest chunk of time.

Step 4: Make an offer and negotiate (up to a week)

If you’re a first-time homebuyer, you might also want to get a sense of how rates fluctuate and the current rate environment so you know what to expect when you seek a quote. You can sign up for a Bankrate account to determine the right time to strike on your mortgage with our daily rate trends. You’ll have to get a loan if you can’t pay cash, so it’s important to ensure your finances are in a good position to handle a mortgage. Andrea Riquier is a New York-based writer covering mortgages and the housing market for Forbes Advisor. She was previously at Dow Jones MarketWatch, on the housing market and financial markets beats. Before that, she covered macro and central banks for Investor's Business Daily, and municipal bonds for Debtwire.

Where Should I Live? 12 Important Factors To Consider

Whether you’re a first-time buyer or looking to make a strategic investment, navigating such a market requires knowledge and careful planning. In this blog, we’ll provide you with step-by-step instructions on how to buy a home in Los Angeles successfully. As you’re getting ready to make an offer on a home, it’s important to understand that there is a decent chance that another buyer might not need to submit any kind of pre-approval documentation. Redfin data shows that 16 percent of purchases in the LA metro area were all-cash deals in the first quarter of 2021. Mortgage preapproval is an in-depth assessment of your homebuying budget, and your lender will pull your credit report and verify your employment status, income, assets and debts.

However, you may be able to become a homeowner in Los Angeles for a much smaller upfront investment. If you have excellent credit and a low debt-to-income ratio, some lenders will offer you conventional loan terms with a down payment of just 3 percent. However, it’s important to understand that a bigger down payment will make a huge difference in your monthly mortgage payment. There are also programs in the Los Angeles area available specifically for first-time buyers. They include California’s first mortgage programs and LA County’s First Home Mortgage Program. Both offer financial assistance to cover down payment and closing costs.

After your home passes inspection and undergoes an appraisal, you’re ready to close. Closing involves signing all the necessary paperwork on your mortgage and taking control of the property. They can help you find a property in your budget and seal the deal at closing. They have your best interests at heart, can advise you on how much to offer for a property and will help you submit an offer letter.

Closing day typically involves a considerable amount of paperwork and can last about an hour or more. As this is one of the final steps to buying a house, you’ll want to make sure there are no questions left unanswered. Work with a homeowners insurance broker to help you determine the type and amount of coverage you need.

Indiana First-Time Home Buyer 2024 Programs and Grants - The Mortgage Reports

Indiana First-Time Home Buyer 2024 Programs and Grants.

Posted: Tue, 23 Apr 2024 07:00:00 GMT [source]

A licensed appraiser will determine the home’s market value based on comparable recent sales of homes in the neighborhood. After the appraisal has been completed, it will typically take around two weeks for the lender to get all the paperwork and approval completed. Buying a house for the first or even second time can be extremely exciting, but it can also be one of the most complex purchases of your life. Not knowing what to do when and how to start can make it even more daunting.

Buying a home with no money down is possible, but most homeowners need to have some cash on hand for a down payment. For example, you may find that you would prefer a single-family home, but the cost in your area stretches your budget to the maximum. You might consider townhomes or condos with similar square footage but at a lower cost, if the HOA fees still make it worth it. First, you’ll find out exactly how much you’ll be able to borrow and therefore, how much home you can afford. Knowing your purchase power will help guide your home search and keep you from unnecessary disappointments that come with shopping outside your limits.

You can use online real estate databases to help you find properties within your budget that fit your needs. Your REALTOR® or real estate agent will be a big help as you look for homes. Divide your total monthly debts by your total monthly pre-tax income to find your DTI ratio. For example, if your total monthly household income is $5,000 and you pay $2,000 a month in recurring expenses, your DTI ratio is 0.40, or 40%. If you’re a first-time home buyer, an organized checklist can help keep you on track as you look toward closing.

Your real estate agent and loan officer will take care of most of the work, but you will have a few final tasks — including signing mountains of paperwork. The credit score required to buy a house depends on your lender and the type of loan you’re taking out. You can expect to qualify for common types of home loans with a credit score of 620. But some lenders will still consider you eligible with a lower score if you exceed other criteria.

Many home buyers believe they need a 20% down payment to buy a home, but this isn’t true. Plus, a down payment of that size isn’t realistic for many first-time home buyers. Fortunately, buyers who can’t afford a 20% down payment have several options, depending on the loan type.

No comments:

Post a Comment